Every budget season, I hear from CFOs who lament the difficulties of creating a break-even budget as divisions across the institution ask for more money to fund new initiatives while no existing activities or costs are eliminated. The assumption seems to be that CFOs can balance a budget alone, but we can’t. This is why setting a three-phase, cascading approach to budgeting is important.

Before we can do this, we need to be clear about two things:

- The bottom line we expect to achieve this year—i.e., our goal—based on the definition of financial sustainability.

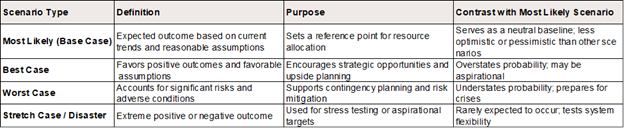

- A common definition of our stance on budgeting. For example, I hear terms like “conservative” or “high, medium, low.” I prefer “most likely.”

“Most Likely” – What does it mean?

A “most likely” budget scenario corresponds with a neutral baseline scenario—neither optimistic nor pessimistic, not conservative or aggressive. It assumes you are not starting or stopping any activity other than those from decisions made previously. It’s generally developed by blending historical expenses, adjusting for inflation (e.g., 3%), and accounting for other decisions and changes that have occurred since last year, such as hiring a new position or starting a new program.

This matters when we work with budget managers and hear them say things like “to be conservative.” I push back on that framing and explain that we don’t want to be conservative. We want to know that, with effort, the goal is achievable.

The importance of “most likely” is clarity. Budget managers often get confused when asked for multiple scenarios (high, medium, low). By focusing on one at a time, we create precise goals and better focus for planning. Of course, adjustments can be made if the revenue goal is different from most likely.

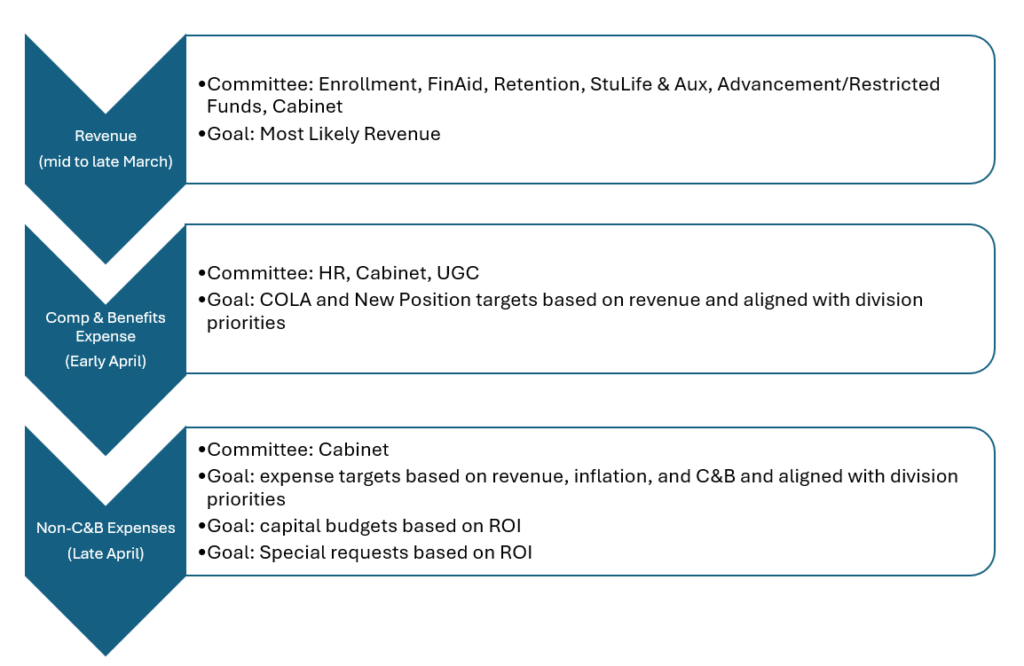

Now, we’re ready to start our three-phase, cascading budget process.

Start With Revenue

The first phase focuses on budgeting “most likely” revenue to understand how much we have to spend, and to set those expectations for budget managers up front. If we ask everyone to budget without that context, nearly every budget will come back with a 3-6% increase over last year. But if our revenue is projected to be flat, we should set expense expectations before the process begins.

It’s critically important that revenue is budgeted at “most likely” to avoid last-minute changes to expense budgets. To achieve this shared understanding, budgeting needs to be a team sport. That means involving enrollment, financial aid, student success, and advancement to ensure that each agrees to the metrics for their division: new students, retention rate, discount rate, percentage of students living on campus, annual fund, and so on. These metrics should not be set by finance; they should be set by the division that owns the responsibility of achieving them.

This allows monthly monitoring of the metrics from the time they’re set to the start of the fall semester. For example, at this time of year, we should be able to see how our deposits and financial aid awards are comparing to last year to gauge whether the revenue budget we’ve set is on track. These metrics should be discussed regularly at cabinet meetings throughout the budget process to ensure shared understanding.

Set Expense Targets

Once revenue is set, we can set expense targets for both compensation and non-compensation line items. For example, if revenue is going up by 2%, that means we only have 2% more to spend on expenses (and potentially less, depending on our financial sustainability goals). We generally have little control over non-compensation expense increases. They’re tied to inflation. This can leave even less room for compensation. If, for example, my compensation increases take effect in January, those costs will rise this year even without any cost-of-living (COLA) increases. That needs to be factored in.

The point is that without adding any additional activities, costs are likely to rise at 3%. If revenue is only rising at 2%, that means we need to find cuts.

These are decisions that should be made jointly with the leadership team, not set by finance. This creates shared ownership of the outcome.

A Real-World Example

I worked with a client who went through this exact exercise and determined that they wanted to take care of the people they had with a COLA increase, even if that meant retaining fewer people. Ultimately, the staff reductions were not significant—some vacant roles were put on hold. After that, the decision was made to reduce non-compensation expenses. (That’s not easy when you’re fighting inflation at the same time.) In this case, each member of the leadership team was asked to come to the table with ideas for a 5% reduction in non-compensation expenses, which the group discussed and debated.

The result: the leadership team owned the budget and understood their role in achieving it. Finance’s goal became what it should be: providing timely, accurate, and meaningful information to help the leadership team monitor their budget.

Of course, all of this should be modified for your institution. But the goal is the same: to create a collaborative process with clear objectives and shared ownership of the budget outcome.